This course id from edX, scroll down & click “Read More” for more informations.

About this course

Blockchain is a core technology in FinTech. The original design of blockchain focused on the cryptocurrency “Bitcoin”. Due to its specific characteristics, many companies and users now find blockchain very useful for applications in many areas, not limited to cybercurrencies, including finance, logistics, insurance, medicine and even music. However, the design of blockchain involves cryptographic technology, which cannot be easily understood by those who are not professionals in the area of IT and security.

In order to better understand what kinds of applications best fit blockchain and other forms of distributed ledger technology and the potentials of these emerging technologies, it is important to understand the design rationale, the basic technology, the underlying cryptographic fundamentals, and its limitations. This 6-week online coursewill walk you through the following:

- The design rationale behind blockchain and the issues for such decentralized ledger (transaction) systems.

- The underlying technology (e.g. how the fundamental algorithms – the cryptographic primitives – work together) behind and how it makes blockchain works and safe.

- The differences of the various existing blockchain platforms and what these platforms can provide (e.g. pros and cons of the major platforms).

- What kinds of applications (both traditional and emerging) best fit the blockchain technology and how blockchain technology can benefit these applications.

- Blockchain does have its limitations. We will uncover the problems and the limitations of blockchain technology to enable developers and researchers to think about how to enhance the existing blockchain technology and practitioners to better address the issues when using blockchains in their applications.

- This course will also briefly discuss the downside of blockchain with respect to the protection of criminal activities (e.g. why ransomware always ask for bitcoins as ransom, and the money laundering problem).

The course aims at targeting a wide audience: This course will provide learners a good understanding of the technological, applicability, limitations and “illegal” usage of the blockchain technology.

What you’ll learn

- Understand the design rationale behind the blockchain technology.

- Understand the technological and cryptographic components of a blockchain.

- Understand the variations and differences of existing major blockchain platforms.

- Understand what types of applications best fit the characteristics of blockchain.

- Understand the limitations and outstanding issues of existing blockchain technology.

- Understand the negative impacts of, in particular, criminal activities in the context of blockchain.

Welcome and Course Administration

Welcome to Blockchain and FinTech: Basics, Application and Limitations

- Hello everybody.

- The upcoming Blockchain and FinTech course

- will be launched in August this year.

- It will be about blockchain technology,

- blockchain platforms, applications and limitations.

- This is a course aimed for layman learners.

- Learners will be able to understand

- the fundamental and industrial jargons,

- so that you can interact with

- key players of the industry.

- I look forward to seeing you

- in the blockchain course.

- The big rise and crash in Bitcoin market

- peaked peoples interest in blockchain technology.

- But, is Bitcoin equivalent to blockchain?

- Of course not.

- Some even think that in the near future,

- this new technology can change the way we live

- and the way we do business.

- In fact, we’ll be expecting

- new business models

- and new business opportunities.

- There’ll even be new ways of

- exchanging information online.

- But do you know what blockchain actually is?

- Take a look at the following questions.

- Do you know much about these?

- Do you know what underlying technologies

- make blockchain secure and powerful?

- What kind of applications,

- both financial related or non-financial

- are best fit for blockchain?

- How do these blockchain platforms differ?

- For example, Bitcoin, Ethereum,

- Hyperledger, Chinaledger?

- Is blockchain 100% secure?

- Can it protect your privacy?

- If not, what kinds of protections are provided?

- Why do ransomware

- request Bitcoin as payment?

- Why do people perceive cyber-currencies

- as a means of money laundering?

- If you want to get more insights,

- join the Blockchain FinTech course.

Course Outline and Syllabus

Introduction to Blockchain and FinTech: Basics, Applications and Limitations – Course Outline

Introduction to Blockchain and FinTech: Basics, Applications and Limitations is a six-week six-module course. Each weekly module compiles 6-12 lesson units (or subsections). In addition to the main units of the lesson, there are also Industry use cases highlighting real world examples and applications from different industry sectors.

The major learning activities within each lesson unit include: video discussions of major aspects with peer learners, instructor and community TA, as well as continuous assessment in the form of Quick Check questions, Polling and Word Cloud activities. In addition to these, there are a range of additional resources provided, including blockchain industry news reports, studies and useful links. There is a Conclusion Quiz at the end of each module to draw out the main messages.

Please click the link to view and download the Course Syllabus.

| Module 1 Blockchain technology: Why, What, How | |

| 1.1.1 | Why Do We Need a Decentralised Ledger System? Part 1 |

| 1.1.2 | Why Do We Need a Decentralised Ledger System? Part 2 |

| 1.2 | Having a Centralised Trusted Party – Advantages and Disadvantages |

| 1.3 | Security, Integrity and Privacy Issues of a Decentralized System |

| 1.4 | Blockchain – A Technology that Makes Sense with Trust and Coordination (An Interview with Charles d’Haussy from ConsenSys) |

| 1.5 | What Are the Main Barriers to Blockchain Adoption? (Charles d’Haussy from ConsenSys) |

| 1.6 | Why Use Blockchain Technology? (Henri Arslanian from PwC) |

| Ref | Reference Videos from Introduction to FinTech |

| Introduction to FinTech Module 2.9A What is Blockchain? (Part 1) | |

| Introduction to FinTech Module 2.9B What is Blockchain? (Part 2) | |

| Module 2 Technological and Cryptographic Elements in Blockchain | |

| 2.1.1 | Cryptographic Elements: Public Key & Private Key |

| 2.1.2 | Cryptographic Elements: Digital Signature & Hash Value |

| 2.1.3 | Cryptographic Elements: Real-life Scenario Challenges |

| 2.2.1 | Cryptographic Technology: Key Questions for Blockchain |

| 2.2.2 | Cryptographic Technology: Who can Modify Transactions? |

| 2.2.3 | Cryptographic Technology: Who will Maintain Transactions? |

| 2.2.4 | Cryptographic Technology: How to Protect Our Privacy? |

| 2.2.5 | Public-key Cryptography (Prasanna Mathiannal from MaGEHold) |

| Module 3 Blockchain Platforms | |

| 3.1.1 | Classification of Blockchain Platforms (Part 1) – An Overview of the 5 Key Perspectives |

| 3.1.2 | Classification of Blockchain Platforms (Part 2) – Perspectives No. 1 and 2 |

| 3.1.3 | Classification of Blockchain Platforms (Part 3) – Perspective No. 3 |

| 3.1.4 | Classification of Blockchain Platforms (Part 4) – Perspectives No. 4 and 5 |

| 3.1.5 | Highlights of Major Blockchain Platforms |

| 3.2.1 | What is Ethereum? (Charles d’Haussy from ConsenSys) |

| 3.2.2 | What is Ethereum’s Place in Today’s FinTech Ecosystem? (Charles d’Haussy from ConsenSys) |

| 3.4.1 | Trustlessness and Immutability of Blockchain Technology (Charles d’Haussy from ConsenSys) |

| 3.4.2 | Proof of Work and Proof of Stake (Charles d’Haussy from ConsenSys) |

| 3.5.1 | Tokenizing (Charles d’Haussy from ConsenSys) |

| 3.5.2 | What is a Token? (Charles d’Haussy from ConsenSys) |

| 3.5.3 | Tokenizing Shares and Fund Raising (Charles d’Haussy from ConsenSys) |

| 3.6 | What is Hyperledger? |

| Module 4 Blockchain Applications | |

| 4.1.1 | 6 Selection Criteria for Blockchain Applications (Part 1) Key Factors 1, 2, 3 |

| 4.1.2 | 6 Selection Criteria for Blockchain Applications (Part 2) Key Factors 4, 5, 6 |

| 4.1.3 | 6 Selection Criteria for Blockchain Applications (Part 3) Best Fit Applications |

| 4.1.4 | 6 Selection Criteria for Blockchain Applications (Part 4) Decision Making |

| 4.2.0 | Blockchain and Enterprise – A Technology of Coordination (Charles d’Haussy from ConsenSys) |

| 4.3.1 | Why Permissioned Blockchains Are Used in Enterprise Network? (Dr. Paul Sin, Consulting Partner from Deloitte, China) |

| 4.3.2 | Use Case: Blockchains for Trade Finance (Dr. Paul Sin, Consulting Partner from Deloitte, China) |

| 4.3.3 | Use Case: Blockchains for Supply Chain Financing (Dr. Paul Sin, Consulting Partner from Deloitte, China) |

| 4.3.4 | Use Case: Cross Border Connectivity – Trusted Data Transfer (Dr. Paul Sin, Consulting Partner from Deloitte, China) |

| 4.4.1 | How to Deploy an Application on the Ethereum Blockchain? (Charles d’Haussy from ConsenSys) |

| 4.4.2 | Use Case: Bounties Award Ethereum for Cleaning Beaches (Charles d’Haussy from ConsenSys) |

| 4.4.3 | ConsenSys and the Ethereum Platform (Charles d’Haussy from ConsenSys) |

| 4.4.4 | ConsenSys Use Case: Project i2i (Charles d’Haussy from ConsenSys) |

| 4.5.1 | Blockchain Use Case: More on Trade Finance and Supply Chain (Anil Kudalkar from MaGESpire Partners) |

| 4.5.2 | Blockchain Use Case: Capital Markets (Anil Kudalkar from MaGESpire Partners) |

| 4.5.3 | Blockchain Use Cases on General Government Services & Sustainable Livelihood (Anil Kudalkar from MaGESpire Partners) |

| Module 5 The Limitations, Opportunities and Challenges of Blockchain | |

| 5.1.1 | 5 modules in Blockchain system |

| 5.1.2 | Limitations of Blockchains (Part 1) |

| 5.1.3 | Limitations of Blockchains (Part 2) |

| 5.2.1 | Risks and Limitations of Blockchain: Privacy (Malcolm Wright from Diginex) |

| 5.2.2 | Risks and Limitations of Blockchain: Security (Malcolm Wright from Diginex) |

| 5.2.3 | The Five Security Risks of Blockchain (Alan Cheung from Hong Kong Applied Science and Technology Research Institute (Astri)) |

| 5.3.1 | Applied Smart Contracts: Opportunities, Risks, and Applications for Enterprise (Jon Rout from Digital Asset) |

| 5.3.2 | Applied Smart Contracts (DAML): Step-by-Step Example (Jon Rout from Digital Asset) |

| 5.4.1 | Use Case: Blockchain for Health Insurance (Alan Cheung from Hong Kong Applied Science and Technology Research Institute (Astri)) |

| 5.4.2 | Use Case: Blockchain & PropTech (Alan Cheung from Hong Kong Applied Science and Technology Research Institute (Astri)) |

| 5.4.3 | What Are the Benefits of Blockchain in Banking? (Johnny Cheung from B.C. Holdings) |

| 5.4.4 | How Can Blockchain Technology Benefit the Healthcare Industry? (Johnny Cheung from B.C. Holdings) |

| 5.4.5 | Institutional Investment Opportunities in the Digital Asset Space (Henri Arslanian from PwC) |

| 5.5.1 | Facebook’s Libra – Development in Blockchain, DLT and Cryptocurrency (Part 1) (Brian Tang from Asia Capital Markets Institute (ACMI)) |

| 5.5.2 | Facebook’s Libra – Development in Blockchain, DLT and Cryptocurrency (Part 2) (Brian Tang from Asia Capital Markets Institute (ACMI)) |

| 5.5.3 | Facebook’s Libra – Development in Blockchain, DLT and Cryptocurrency (Part 3) (Brian Tang from Asia Capital Markets Institute (ACMI)) |

| 5.5.4 | Facebook’s Libra – Development in Blockchain, DLT and Cryptocurrency (Part 4) (Brian Tang from Asia Capital Markets Institute (ACMI)) |

| Module 6 The “Evil Sides” of Blockchain and Legal Regulations for Blockchain | |

| 6.1.1 | The Evil Sides of Blockchains Part 1 Ransomware |

| 6.1.2 | The Evil Sides of Blockchains Part 2: Money Laundering |

| 6.1.3 | The Evil Sides of Blockchains Part 3: Cyber Currencies |

| 6.1.4 | The Evil Sides of Blockchains Part 4 Cyber Security Exchanges |

| 6.2 | The “Dark” Side of Blockchain (Bowie Lau from MaGESPire) |

| 6.3 | Criminal Use of Payment Blockchains (Malcolm Wright from Diginex) |

| 6.4 | The Role of Financial Regulations for Blockchain (Professor Douglas Arner, Faculty of Law at the University of Hong Kong) |

| 6.5 | Does Blockchain Need Legal Regulations? (An Interview with Charles d’Haussy) |

| 6.6 | Global Digital Assets Regulatory Trends (Henri Arslanian from PwC) |

Module 1 Blockchain Technology: Why, What and How

Welcome to Module 1

Meet Module 1 Guest Speakers

Module 1 Learning Objectives

After completing Module 1, learners should be able to:

- Understand the differences between a distributed system and a decentralised system;

- Understand the advantages and disadvantages of having a centralised trusted party to process and store transaction data of an application;

- Understand the advantages and issues to be resolved of a decentralised system.

Think about this

Do you know the difference between a “decentralised” and “distributed” systems?

Why do we need a decentralised ledger?

Why Do We Need a Decentralised Ledger System? (Part 1)

- Before we start,

- there are two terms I want to clarify.

- You always see these terms in the internet.

- One is called decentralised system.

- The other is distributed system.

- Distributed system actually refers to

- a system that can store or process data

- in different locations.

- But whether it is a decentralised system,

- depends on how and where

- the decision making is made.

- Decentralised essentially means

- there’s no single point or single party

- who can make the final decision

- of how the system behaves.

- So, every party can make a decision

- for its own behaviour,

- and the resulting behaviour of the whole system

- will be the aggregate responses

- from the individual parties.

- Simply speaking, decentralised means

- that there’s no single authority

- who can control or decide what the system should do.

- In contrast, you can imagine Google search engine

- is basically a distributed system,

- but is not decentralised.

- It still relies on thousands of computers

- in different locations to check the web,

- to crawl the web

- from different locations of the world,

- but then the whole system is owned

- and controlled by Google.

- So, in other words, Google is the only organisation,

- only party who can control the whole system.

- So, that’s why it’s not qualified

- as a decentralised system.

- Now, then the immediate follow-up question is:

- Why do we need a decentralised ledger system?

- Before I talk about this,

- let’s look at the history.

- Let’s start at the very beginning.

- Why do we need banks?

- We need banks because we need a trusted organisation

- to help us to store our money.

- Otherwise, it’s really dangerous

- to keep our money at home.

- The bank, as a centralised trust party,

- will keep track of all our money accounts

- of all the customers.

- In other words, the bank will keep a centralised ledger

- for all these accounts.

- And the bank is the only one who is responsible

- for the integrity and validity,

- that is, the correctness of all the transactions

- in these accounts.

- Let me give you an example.

- If a Person A wants to transfer $100

- to a Person B, the bank will try to track

- if A has enough money in his bank account

- before allowing the transaction.

- And of course, the bank will also try to mark down

- this transaction clearly in the ledger if it’s completed.

- And both the party A and B

- will not have any worry about if the transaction is faked

- because we all trust the bank.

- Now but then, why the bank is willing to do this for us?

- The bank can actually make use of our money

- to invest and try to earn more money on their own.

- That’s why they are willing to provide this service for us.

- Now, in order to attract more customers

- to deposit the money in the bank,

- the bank will give the customers interest in return.

- So, it is basically the relationship

- between the customer and the bank.

- So far so good, right?

- The customer right now has a trusted party, the bank,

- to help handle his money account

- with the benefit of getting interest as well.

- Now, on the other hand, the bank can make use of

- the customer’s money to make more money.

- As time went by, the services or the funds

- of the bank has evolved a lot.

- If you look at the current situation,

- there’re many, many services

- provided by the bank now,

- for example, bank loans, money exchange,

- inter-bank transfer, electronic money transfer,

- auto pay or even investment.

- So, it seems like we are having

- such a centralised authority,

- it’s very good.

- However, let’s now take a closer look at this

- to see if it’s really that good

- to have a centralised party helping us

- with all these transactions.

1.1.2 Why Do We Need a Decentralised Ledger System? (Part 2)

- First, you all know that

- these services may not come for free.

- We probably have to pay transaction fees.

- For example, is some countries we need to pay charges

- when we are using ATM transactions,

- cashier’s cheques, money orders, bounced cheques

- wire transfer, safety box, investment transaction,

- or even they impose a minimum balance in the account,

- otherwise, you have to pay a charge.

- Pick the wire transfer as an example.

- If you have a son studying abroad in the U.S.,

- you want to send him some money

- from Hong Kong to the U.S.

- both the banks in Hong Kong and the U.S.

- will charge you a transaction fee.

- They may also have minimum

- or maximum requirements

- on the amount of money that can be transferred.

- Now, having a middle man,

- a trusted centralised party

- for transactions and business is not uncommon

- in the real world.

- There are many, many examples.

- Now, let’s try to look at a few.

- In China, there’s a place called Guiyang.

- They established something called

- the Global Big Data Exchange.

- This exchange has been established

- for three years already.

- It provides a centralised platform for the customer

- to trade, buy and sell the data.

- So, basically it’s a data trading centre.

- How it works, the data owners deposit their data

- into the platform just like what we do for the bank.

- We deposit the money in the bank.

- And the buyers could go to the platform

- and try to purchase the selected data from the platform,

- based on what data are provided by the data owner

- and what data will be required by the buyers.

- And the centralised party,

- the platform, will try to coordinate

- this buying and selling activities or provide services

- to help match the buyers and sellers.

- You all know it, right?

- Of course, the service is not for free.

- The platform charges a transaction fee.

- The transaction fee can be as high as

- 40% of the whole transaction amount.

- For example, if you are going to pay $1,000

- to buy and sell data,

- you are going to pay $400 to the platform.

- Now this is only one example.

- There are many, many other examples.

- Let me give you another remarkable example.

- Matchmaking service is very common now.

- You can see that the company,

- the platform providing this service,

- can be considered as our centralised trusted party,

- and of course the service is not for free.

- To use the service,

- to find the potential dating partners or candidates,

- in most cases,

- a customer has to pay membership fee

- and, if they successfully arrange a dinner

- for you and the potential candidate,

- they may even charge you another service charge.

- Think about it.

- If it’s possible to eliminate the centralised party,

- we may not need to pay this transaction fee.

- Now, in fact, having a centralised party

- to look after our transaction

- also comes with the privacy issues.

- It’s very obvious that

- the bank, the centralised party, the platform,

- is able to look at all your transactions.

- For example, to whom you want to give your money to,

- how much money you have exchanged

- for foreign currencies,

- how much money you have wired to your children,

- and of course, all of your investment via the bank.

- If you look at the love matching example,

- the privacy issue is quite obvious, right?

- Because you need to pass your personal information

- to the platform and also the criteria

- for choosing your partner, for example,

- what kind of girls you like, etc, and of the privacy,

- you totally rely on the service provider.

- And this service provider

- will have full access to the information,

- which couples have communicated

- and when and where they go for dinner

- and who want to date which one.

- And, of course, you may not even want others to know

- that you have register for this kind of service.

- And for the big data exchange example,

- there are also some privacy issues.

- The platform, because you deposit your data over there,

- so the platform has all the authority

- to look at every single piece of data,

- and there is no absolute guarantee

- that the platform will not use your data

- for other purposes.

- And, of course, the platform also know

- every single transaction of every trade,

- who buys a piece of data, who sells it, who owns it

- or for how much the data was sold.

- Sometimes, time is also a concern

- because we have to rely on the centralised party

- to process the transaction.

- In most of the cases, it will take time.

- For example, if you want do a wire transfer

- to someone in another country,

- it may take the bank days to complete the transaction.

- And the bank probably may also have other restrictions,

- for example, they may have a restriction

- on the minimum or maximum amount

- that you can transfer for one time.

- And depending on the nature of the transaction

- and/or the applications,

- some transactions may involve multiple parties

- and many steps in the procedures.

- As a simple example,

- let’s consider a mortgage loan.

- From the time you want to apply for a mortgage loan

- till you really get the mortgage loan,

- maybe you have the experience.

- It will take more than 20 days, or a few weeks, right?

- In fact, inside this process,

- there are many parties to be involved.

- For example, the borrowers need to work with

- different parties to provide proofs of his salary,

- his employment, his credit history, etc,

- And the bank may also need to work with

- many other parties, for example, surveyors

- to evaluate the property for the loan

- based on the current market price.

- And the bank may also need to

- interact with other parties,

- such as the land registry

- to verify the ownership of the property.

- Then, you can imagine that

- everything goes back to the centralised party,

- that’s the bank in our case,

- then it would become the bottleneck of the procedure.

- And, of course, if you want to look for a mortgage loan,

- you are not going to ask a single bank to do it.

- Usually we try to seek services

- or make enquiries from multiple banks.

- And of course the banks will not work together.

- They will not share information at all.

- So, it creates a lot of redundancy

- in the transactions as well.

- Now, you think about it.

- Imagine that if there’s a platform in which

- some information is given access to every bank

- if the customer agrees,

- the validation process of opening a bank account

- in different banks for the same customer

- would be a lot easier,

- and you can save a lot of time.

- But if we are having the concept

- of a centralised system,

- this platform is not easy to build

- because no one is going to trust one single authority

- who have full control of this platform

- with the exception of the government.

- In other words,

- it’s not easy to have a commonly trusted party

- to manage the operation of the system.

- If you can follow what we have discussed so far,

- you may wonder is it possible to do all these

- without a centralised party?

- For example, without a bank,

- you know, this is the reason why blockchain

- or a decentralised ledger system was proposed.

- But on the other hand,

- not all applications or systems are suitable to be a kind.

- We’ve also discussed what kind of applications

- are best fit for decentralised systems

- in the later part of the course.

Think about this

Banking transactions demand adequate security. What are the advantages and disadvantages of a centralised and decentralised system in bank services such as payment and remittance?

1.2 Having a Centralised Trusted Party – Advantages and Disadvantages

- I hope you are now convinced

- why we need a decentralised system.

- However, a decentralised system

- is not owned by anyone

- but by all the users who use the system,

- so in other words

- all the users of the system

- have to work together

- to maintain the whole system

- so the big question is,

- is it really feasible?

- What will be the issues there?

- To understand the issues

- of building a decentralised system

- for an application,

- let’s try to look at the bank accounts

- as an example.

- Now assume that

- we have already opened an account in a bank.

- We have mentioned that the bank can help us

- to maintain our account ledgers,

- deposit money into the account,

- withdraw money from the account

- and transfer some money from one account

- to another account.

- Now imagine that I try to deposit 15 coins

- into my own account.

- The bank provides you a deposit slip

- and the account balance is recorded.

- Now on the other hand,

- if you do not have a bank,

- how can you confirm

- that you have actually deposit 15 coins

- into the account?

- Another example.

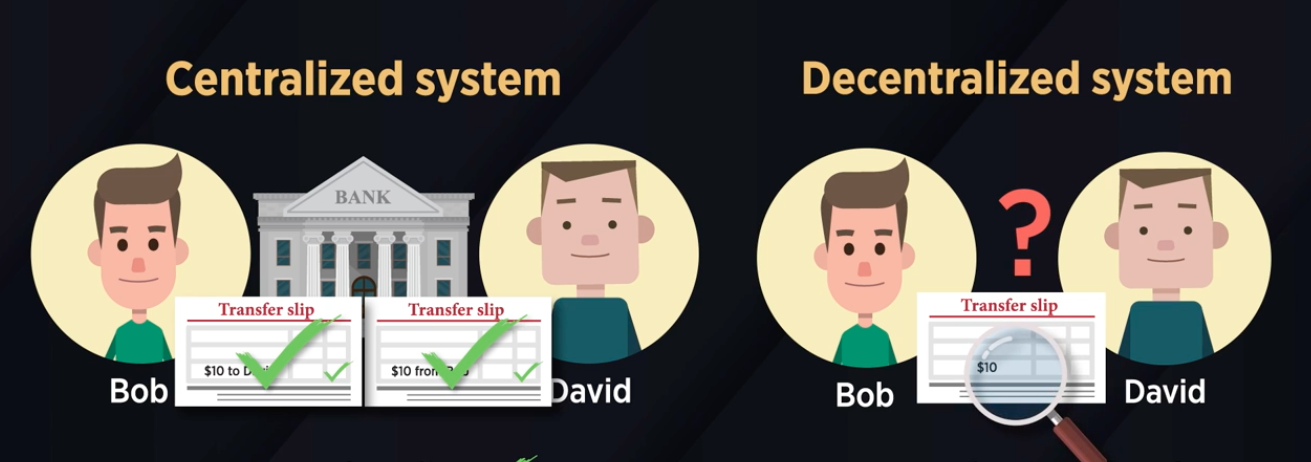

- If Bob wants to transfer 10 coins to David

- with a bank, you can sign a transfer slip

- to authorise it and both you and Bob

- has no doubt about the transfer.

- The bank has processed it.

- However, if we don’t have a bank,

- how can one authorise the transfer?

- How can one check if the transaction is valid?

- In other words,

- how can we guarantee that Bob

- has 10 coins in the account

- so that he can transfer the coins to David?

- Now with a centralised party,

- the bank will keep track

- of all transactions for its customers

- and account balance for its customers,

- so if one person wants to transfer

- a certain amount to another account,

- the bank will verify if the person

- has enough money to do so or not,

- but then if you’re without a bank,

- without a centralised party,

- how can this be done?

- One simple solution is

- how about we just put

- all the transaction details,

- all our accounts on the internet.

- Then everybody can get a copy

- and help to check it.

- Now if A wants to transfer $60 to B,

- then everybody can see whether A has enough money

- in the account

- and whether the transfer can be done legitimately

- and of course now that the transaction has been done,

- a new record of the transaction can be written

- on the internet-based ledger as well.

- Then both A and B can see clearly the changes

- in the account and the transaction can be done

- very fast too.

- Since we put all the details

- of all the transactions and the accounts on the internet

- so everybody can check it

- and all actions are transparent, am I right?

- But the problem is in the bank,

- the bank will be responsible for all the accounts,

- all the transactions.

- More importantly the transaction details

- and the accounts are kept by the bank

- and the bank can make sure

- that nobody, no unauthorised people

- can modify the transaction

- or the account can easily be changed.

- But now the whole ledger is available

- in the internet, everybody is authorised

- has the right to download a copy,

- so can anybody modify the transaction easily?

- Do we have a mechanism to make sure

- that this is not possible?

- Or can anyone add/delete transactions easily?

- How to give the authorization

- to transfer money from your account

- to another account,

- who actually is responsible to maintain the account?

- Maintain the ledger?

- Who’s going to check the validity of a transaction?

- You see there are many, many problems.

1.3 Security, Integrity and Privacy Issues of a Decentralised System

- Now, let’s try to talk about the issues in more detail.

- To make it very simple, if it’s very easy for one

- to modify the transaction details,

- then the system becomes useless

- because we cannot trust

- the ledger that we download from the internet.

- For example, if I transfer $10 to B today,

- but then, tomorrow, I don’t want to transfer

- the money to B, so what can I do?

- I go to the internet,

- download the ledger, erase my record,

- or even say that B actually transferred $6 to me instead.

- Then, I put the ledger back in the internet.

- Then, everybody will download my new ledger

- and think that B actually transferred

- $6 to me instead of I transfer $10 to B.

- Then, you can see that the system becomes useless.

- Nobody’s going to trust it.

- So how to guarantee that only the account owner

- can initiate a transaction of his own money?

- This is actually a security issue.

- Now, if it cannot guarantee

- the transactions are error-free,

- for example, if the transaction is transferred

- even if the paying account

- does not have enough money,

- then we will think that the system is useless as well.

- Therefore, you can imagine that integrity

- is really, really a big issue.

- So whether we can trust the transaction detail

- on the internet is of question.

- Now, of course,

- you can see that with a centralised system,

- the bank can check every transaction,

- whether it’s valid or not, but in a decentralised system,

- everybody’s an owner.

- We don’t know who is going to check

- if the transaction is valid.

- This is also an integrity issue.

- Now, if the ledger is maintained

- by all users, so everybody may get a copy.

- So if some problems occur,

- which copy is the correct one?

- Which copy can we trust?

- You can see that there are many, many questions

- related to security and integrity.

- In fact, who is responsible for adding new transactions

- into this global ledger is also an issue,

- is also a problem.

- Now, if you look at it very carefully,

- there’s one more important question.

- If you put everything on the internet,

- every transaction on the internet,

- so everybody can have the authority to look

- at all the details, all the accounts, all the transactions,

- as they are all the owners of the platform,

- then it seems like the protection of privacy

- in comparison to a bank is even worse.

- You think about it.

- In case of a bank, only the bank can look

- at all the transactions for its customers,

- but in a decentralised system,

- it seems like everybody can

- go to the blockchain platform

- and look at all the transactions.

- Now, I hope you learned enough to understand that if

- we are going to have a decentralised system,

- there are many, many issues to be resolved.

- Okay, let me summarise the lecture of this module.

- Now, if we are going to have a centralised party,

- like a bank, to help us to keep our money,

- there are some disadvantages,

- such as we need to pay high transaction fee,

- the privacy concern because the bank

- can know everything about us, about the transactions,

- and also the processing time

- may depend on the centralised party,

- and if we are going for multiple parties,

- multiple service providers, you may need to repeat

- the same tedious procedures for every provider

- because they don’t share information.

- Now, on the other hand,

- if we try to go for a distributed ledger,

- the ledger is going to be maintained by all users

- and we may have other concerns

- to maintain the system,

- such as security, integrity, and a privacy issue.

- Now, in the next lecture, we’ll try to take a closer look

- at the blockchain technology

- on how these issues can be resolved.

Meet Guest Instructor Charles d’Haussy (ConsenSys)

1.4 Blockchain – A Technology that Makes Sense with Trust and Coordination (An Interview with Charles d’Haussy from ConsenSys)

- I would like to give you my definition of blockchain,

- because blockchain is a very complex technology

- and it makes it a very difficult technology

- to explain sometime.

- So, some people go in the technical explanations,

- explaining to user,

- there’s a distributed ledger infrastructure

- as information is shared.

- But when you talk to a large audience,

- it’s actually hard for the people to start to picture

- what is this flow of information.

- So the way I like to explain,

- what is blockchain technology,

- is really to explain that

- it is a technology about coordination.

- It’s a technology helping people,

- helping organisations to organise themselves

- in a trustless manner.

- And if you’re a technical person,

- we can talk about the ledger,

- as in the way the information is encrypted

- and shared between different databases.

- But the overall takeaway,

- it’s a technology which never exists before,

- and it’s a technology which main objective

- is to help coordination.

- So the worst case of blockchain

- is trying to use blockchain

- for the sake of using blockchain,

- for every use case you want to address,

- you can always execute them

- without using blockchain.

- A central database is always possible.

- But if you want start to coordinate work

- between many, many more parties,

- and you want these parties to have a platform

- which is a trust.

- So they don’t have to trust one single player,

- but they can start to trust each other,

- then blockchain start to make sense.

- So I think a blockchain which is centralising things,

- but still using the blockchain

- for distributing things

- do not capture all the value proposition

- of the blockchain technology.

- So you really want to have a use case

- where there is so many different parties

- with such a complex coordination work

- that a blockchain will actually makes sense

- because it will be easy

- for the platform to onboard them,

- and it will be also making everyone comfortable

- to work that if you claim something

- or if you owe me something

- because I deliver your work,

- the platform is actually coordinating this work,

- and I do not need to have such a high level

- of trust with you, if I deliver a work,

- if I deliver something to you,

- I knew I’m going to be paid

- because I will trust the platform itself.

- So to speak, to the idea of having a distributed ledger

- or blockchain being distributed,

- what’s decentralisation and does it matter

- if a blockchain is decentralised or not?

- So, decentralisation is one of the value proposition

- of the blockchain’s technologies, right?

- In some cases you want to decentralise

- between a short, a small group of players,

- maybe between a bank and their customers,

- maybe between different banks

- or maybe different organisations.

- In this case, you decentralise,

- but you kind of not totally decentralise.

- So it should not be an obsession.

- Decentralisation makes sense,

- but it should not be the only obsession.

- I think we always have to come back to the problem

- you want to fix.

- You want to come back

- if you design a product

- to make sure that this product has a fit

- with the market and start your kind

- of product design journey from the customer

- and not from the technology capacities.

What Are the Main Barriers to Blockchain Adoption? (Charles d’Haussy from ConsenSys)

- So what are the main barriers

- to blockchain adoption?

- The main barriers to blockchain adoption today

- would be defining

- and launching the right products.

- Everyone is experimenting a lot on this ecosystem,

- and we see some use cases

- which are getting traction.

- So the financial use cases are

- getting a lot of tractions.

- Identity use cases

- starting to have a lot of attention.

- What we find is when there is technologies,

- the technologies are way faster than people.

- If you think of the use of the internet back in the ’90s,

- people at the beginning were very scared of the internet.

- I remember people telling me

- I will never use my credit card on the internet.

- And nowadays everyone uses credit card

- on the internet,

- because the people and the habits of the people

- have been changing.

- So today the technology is here,

- the technology is ready,

- the technology is evolving and growing every day,

- but it’s kind of practised by

- a small circle of technologists.

- And step by step, we see

- more and more people using

- these technologies

- sometimes without even knowing.

- If you think about the CryptoKitties,

- the CryptoKitties users and

- fans are not all technologists.

- They’re realising there is new type of products,

- there is new type of online interactions

- and online gaming happening.

- But slowly, slowly the use of

- the blockchain products is expanding.

- So the technology is always faster than people.

- So we have to be patient and always fine-tuning

- and finding the right products

- which will drive the adoption.

Meet Guest Instructor Henry Arslanian (PcW)

1.6 Why Use Blockchain Technology? (Henri Arslanian from PwC)

- Hi there, very excited to be there.

- As most of you know, my name is Henri Arslanian

- and really my passion and my focus in life

- is the future of the financial service industry.

- Ok, now you may be wondering

- what’s happening with blockchain,

- and when it comes to institutional players.

- Well, there’s also a lot of activity there as well.

- For example, the vast majority

- of financial institutions around the world now

- are working on some kind of blockchains.

- And there’s many inherent advantages.

- For example, a lot of the benefits,

- like transparency, traceability, immutability,

- are actually very beneficial in many use cases.

- However, we are still at the early days

- when it comes to blockchain technology

- becoming mainstream.

- For example, a lot of financial institutions today

- are still at the experimentation level.

- They are doing what we call proof of concept (PoC)

- pilots potentially.

- But very few are moving it to production,

- or using blockchain inside

- their current infrastructure.

- There’s numerous use cases going on right now

- in the world that are very, very interesting.

- Not only issues like digital identity.

- Imagine if you’re able to

- put your identity on the blockchain,

- and then you can let people

- access it as you want it or not.

- Or remittance, like we discussed.

- If you want to send money back home,

- or supply chains, smart contracts, trade finance,

- the list goes on and on.

- Let me cover some of them in more detail.

- For example, let’s start with one

- that is a big problem today, supply chain.

- Think about elements like diamonds,

- or elements like, you know,

- companies like Walmart

- or other big grocery stores,

- who want to track where their food is coming.

- We’re seeing now increasingly use cases

- where people are using it for food traceability.

- For example, if you’re a young mom in Shanghai,

- who wants to go buy their milk at a grocery store,

- you want to make sure

- that it’s actually coming

- from that farm in New Zealand

- you believe it comes from.

- And blockchain actually enables us

- to these traceability opportunities.

- But also, imagine

- if you’re buying a diamond,

- for a close friend, for your future wife, or whatever.

- You want to be able to trace that diamond

- is not a blood diamond,

- that it actually had a source,

- you know where it was coming,

- there was no human trafficking involved.

- And blockchain technology enables this,

- and we’re going to see over

- the next couple of years

- a number of use cases

- when it comes to traceability.

- Another one is smart contracts.

- This has been very interesting as well.

- The beauty of a smart contracts

- within blockchain technology

- enables you to actually code a language

- inside the smart contracts,

- and whenever you have an independent event

- that is happening, you have basically

- the contract operates on its own.

- A great example of this was

- in the insurance sector.

- One of the large insurance companies in Europe,

- launched a test, AXA,

- where they did kind of a flight insurance

- on flight delays.

- All flight times, arrival times

- and take-off times are all public,

- so whenever the flight was

- delayed more than two hours,

- automatically, you can get paid for

- your insurance payment on the spot.

- And then there’s many other use cases.

- For example, we look at the remittance space.

- For me personally, it really bothers me

- to see how much fees are still paid

- every year in remittance,

- especially by those

- who cannot afford them,

- who can afford the least.

- The beauty with blockchain technology

- now is we’re really having

- more and more mainstream cases

- of how we can use blockchain technology,

- but especially digital currencies,

- in facilitating these cross border

- payments and remittances.

- But then again, we have a lot of challenges.

- Make no mistake, implementing

- blockchain technology is not easy.

- For example, in many cases it’s still

- quite costly to actually implement it.

- The other big thing is, as is often

- in many cases, still we are not seeing

- direct cost reduction or cost savings.

- One of the reasons for that

- is actually cloud offerings

- are becoming increasingly cheaper,

- and in many cases

- have a lot of security features

- that are available as well.

- Another big challenge is scalability.

- Think if you’re a large company

- that has operations in 150 or 200 countries,

- and over a billion customers.

- You need to be able to use some technology

- that is very scalable.

- And this is actually one of the challenges

- we see with some blockchains,

- is actually that they have scalability limits.

- That they are not able to process

- as many transactions every second

- as many were expected.

- The other big difficulty

- is actually regulatory uncertainty.

- You know, unless you are able to get

- some regulatory clarity,

- many traditional financial institutions

- are reluctant to get more involved,

- because they don’t know

- how regulators will react.

- A final last one,

- last trend that we are seeing

- when it comes to blockchain adoption,

- it really depends on the people

- inside your organisation.

- For example, you know, if you are

- 6 months away from retirement,

- and you don’t want to rock the boat too much

- and shake things up too much before you retire,

- you are unlikely to come and pitch for blockchain

- to be implemented inside your organisation.

- So it really depends on where people are.

- These are risky projects.

- Anybody who has done any kind of deployment

- of a new technology inside of financial institutions

- knows how difficult it is,

- and how risky it is,

- and if it goes wrong,

- normally somebody gets fired.

- So there’s been in this current environment,

- what is actually less and less banking jobs,

- that are generally quite well paid,

- a lot of people are becoming

- a bit more risk averse,

- to actually push some of these innovations

- like blockchain in it as well.

- In many cases,

- we have seen some innovation teams

- take the lead.

- But again, the problem that has been there

- is that innovation teams are often great,

- but they are great for

- public relations perspective,

- for marketing purposes,

- to do some of the initial experimentation.

- But again, when you want to

- have it deployed at scale,

- you need to have the whole

- broader organisation involved,

- from IT to compliance,

- to the management, to finance,

- to bring these things forward

- from that perspective.

- But again, a lot of exciting things

- are going on when it comes to blockchain

- in financial institutions.

- Again, a lot of activity,

- a lot of developments are going on,

- and this is one of the most exciting times

- to be in finance.

- Not only because of

- blockchain and digital assets,

- but because of all of these changes

- we’re going through right now in the world.

- That’s all, my Fam folks.

- Thank you very much.

- It was a pleasure sharing with you all.

*Reference Videos What is Blockchain? [Introduction to FinTech Video 2.9A) by Professor Douglas Arner

- Cryptocurrencies, blockchain, ICOs.

- These are three terms

- that are in the headlines daily all over the world.

- Blockchain is the underlying technology

- which came to prominence with

- the launch of Bitcoin in 2009,

- but what is blockchain?

- Blockchain combines two long-standing

- technological developments.

- On one side, distributed ledger technology,

- and on the other, cryptography.

- If we look at Bitcoin, if we look at cryptocurrencies,

- cryptocurrencies at their base

- are blockchain systems combining

- distributed ledger systems and cryptography.

- Distributed ledger system,

- what is a distributed ledger system?

- For a system like Bitcoin,

- the distributed ledger

- means that the information in the system

- are not stored in one single place.

- Rather, they exist in multiple locations,

- multiple identical ledgers

- throughout the users of the system.

- So, if we think about this idea of ledgers,

- the traditional example is to think

- of something like a bank.

- A bank is a place where

- a certain amount of money is stored,

- it is a single place,

- it is a silo, it is a single ledger.

- At the other extreme, are distributed ledgers.

- Distributed ledgers mean that there is no single place

- where the information, the valuables,

- the data are stored,

- rather they are stored

- across a variety of identical locations.

- In between these structures of

- centralised and distributed,

- we also have network-based structures

- where perhaps you have a single centralised structure

- and a variety of spokes,

- a hub and spoke structure

- whereby the individual spokes connect to the hub.

- So, distributed ledger technology

- combined with cryptography.

- Cryptography is a technology that involves

- the secure storage,

- the encryption of information.

- It has a very long history with important points

- going back to code breaking,

- particularly in the Second World War.

- If we combine distributed ledger technology

- with cryptography, we have a system

- of secure distributed ledgers

- where entries have to be proven,

- proven through the use of a variety of structures

- which then encrypt the data into blocks.

- So, transactions 1 through 50,

- packaged in a block, encrypted together.

- The next set of transactions build on that first block,

- transactions 51 through 100

- encrypted as a second block.

- This structure provides

- a number of very important attributes

- to a blockchain-based system.

- In particular, it provides for security.

- The layers of cryptography across multiple blocks

- make it very hard, but importantly not impossible,

- to necessarily break those blocks

- making blockchain potentially a highly secure system.

- Second, it’s a permanent system.

- In other words, each of those transactions

- is recorded permanently in each of those blocks.

- That means that there is always a traceable history

- of all of the financial transactions

- going back to the very beginning.

- So, with each Bitcoin,

- you can trace back the life of that Bitcoin

- from it’s creation and into each account

- that it has been transferred to over time.

- And finally, transparency.

- Transparency means that the combination of visibility

- allows you to see what is happening in the blockchain.

- This combination of security, permanence,

- transparency, makes blockchain a potentially

- very powerful platform technology

- across a number of areas.

*Reference Video What is Blockchain? [Introduction to FinTech Videos 2.9B) by Professor Douglas Arner

- Cryptocurrencies, blockchain, ICOs.

- These are three terms

- that are in the headlines daily all over the world.

- Blockchain is the underlying technology

- which came to prominence with

- the launch of Bitcoin in 2009,

- but what is blockchain?

- Blockchain combines two long-standing

- technological developments.

- On one side, distributed ledger technology,

- and on the other, cryptography.

- If we look at Bitcoin, if we look at cryptocurrencies,

- cryptocurrencies at their base

- are blockchain systems combining

- distributed ledger systems and cryptography.

- Distributed ledger system,

- what is a distributed ledger system?

- For a system like Bitcoin,

- the distributed ledger

- means that the information in the system

- are not stored in one single place.

- Rather, they exist in multiple locations,

- multiple identical ledgers

- throughout the users of the system.

- So, if we think about this idea of ledgers,

- the traditional example is to think

- of something like a bank.

- A bank is a place where

- a certain amount of money is stored,

- it is a single place,

- it is a silo, it is a single ledger.

- At the other extreme, are distributed ledgers.

- Distributed ledgers mean that there is no single place

- where the information, the valuables,

- the data are stored,

- rather they are stored

- across a variety of identical locations.

- In between these structures of

- centralised and distributed,

- we also have network-based structures

- where perhaps you have a single centralised structure

- and a variety of spokes,

- a hub and spoke structure

- whereby the individual spokes connect to the hub.

- So, distributed ledger technology

- combined with cryptography.

- Cryptography is a technology that involves

- the secure storage,

- the encryption of information.

- It has a very long history with important points

- going back to code breaking,

- particularly in the Second World War.

- If we combine distributed ledger technology

- with cryptography, we have a system

- of secure distributed ledgers

- where entries have to be proven,

- proven through the use of a variety of structures

- which then encrypt the data into blocks.

- So, transactions 1 through 50,

- packaged in a block, encrypted together.

- The next set of transactions build on that first block,

- transactions 51 through 100

- encrypted as a second block.

- This structure provides

- a number of very important attributes

- to a blockchain-based system.

- In particular, it provides for security.

- The layers of cryptography across multiple blocks

- make it very hard, but importantly not impossible,

- to necessarily break those blocks

- making blockchain potentially a highly secure system.

- Second, it’s a permanent system.

- In other words, each of those transactions

- is recorded permanently in each of those blocks.

- That means that there is always a traceable history

- of all of the financial transactions

- going back to the very beginning.

- So, with each Bitcoin,

- you can trace back the life of that Bitcoin

- from it’s creation and into each account

- that it has been transferred to over time.

- And finally, transparency.

- Transparency means that the combination of visibility

- allows you to see what is happening in the blockchain.

- This combination of security, permanence,

- transparency, makes blockchain a potentially

- very powerful platform technology

- across a number of areas.

*Reference Video What is Blockchain? [Introduction to FinTech Videos 2.9B) by Professor Douglas Arner

- Now, if we look at blockchains,

- within this general structure

- we will often have a third level added.

- So, DLT plus cryptography plus smart contracts.

- What are smart contracts?

- Smart contracts are automated systems

- that on the occurrence of pre-determined actions

- something else happens.

- If I provide A, you provide B

- we pre-agree that A and B will be added together

- to create a new C,

- and this occurs on an automatic basis,

- this is a smart contract.

- There is an old joke that smart contracts

- are neither smart nor contracts,

- they are not smart because they are automated,

- they happen automatically,

- on the occurrence of something / events.

- And they are not necessarily contracts,

- but that is a more complicated legal question for later.

- Within this idea of blockchain,

- we can also add in a second important determination.

- Blockchains can either be

- permissionless, or permissioned.

- A permissionless blockchain, like bitcoin,

- means that it is open,

- anyone can participate that downloads the software.

- You download the software, you become a node,

- you’ll have a full picture of the ledger,

- that distributed ledger is distributed to your node,

- anyone can enter.

- But, we also have what are called

- permissioned blockchains.

- A permissioned blockchain,

- involves requirements or governance structures

- or restrictions on entry.

- In other words, only individuals or organisations

- or computers or devices which have been pre-approved

- can join into the network,

- can access the information

- and can potentially contribute transactions.

- Now, when we think about blockchain,

- it may or may not involve cryptocurrencies.

- A cryptocurrency will involve a blockchain,

- but a blockchain does not necessarily

- involve a cryptocurrency.

- In other words if we think of a blockchain based system

- at its base, it is a distributed ledger

- which is encrypted, maybe with an additional layer

- of smart contracts on top.

- Those individual data entries, can be anything.

- The communications between those data entries

- do not necessarily involve any sort of currency.

- One of the most interesting and powerful applications

- for this sort of thing,

- is in production processes,

- the food market where the providence of a chicken,

- or a bottle of whiskey

- can be proven by the blockchain system

- from its creation, its history, its movements

- documented throughout that system.

- So, any eventual possessor

- can document both the origin

- as well as the lifespan of that particular chicken,

- bottle of whiskey, diamond, artwork,

- whatever it may be.

- And that is the real power of blockchain.

- To build systems

- which are potentially highly secure,

- permanent and highly transparent.

- But, blockchain is not the solution

- for every problem, why?

- Because not every blockchain is created equally.

- not every blockchain is necessarily secure.

- Big blockchain systems like Ethereum or Hyperledger

- or R3’s quarter, or bitcoin,

- these are highly secure.

- But if I create a blockchain in my basement,

- probably not that secure.

- Just because it’s a blockchain, doesn’t mean it’s secure.

- Second, from the standpoint of

- permanence and transparency,

- this raises two problems.

- One, is the garbage in, garbage out problem

- in other words if you put that information in,

- it’s in there forever, and that is a big problem

- in the context of building histories,

- building information, the permanence problem.

- And finally, privacy concerns.

- If information goes into,

- a permissionless public blockchain,

- that information may be permanently

- on public display and access,

- and this can create all sorts of problems

- in that not necessarily do we want

- every piece of information permanently on view.

- So, looking at blockchain,

- and this is something that we talk about

- a great deal throughout this course,

- and in other courses.

- Blockchain is a very important technology,

- being used across all aspects

- of the financial sector and beyond.

- But it’s not the solution for every problem,

- but it is giving us an excuse to re-look,

- to reconsider many of our existing systems

- and infrastructure to build better systems.

- (upbeat music)

Module 1 Reference Reading

References and Suggestions for Further Reading in Module 1

(1) Differences between a distributed system and a decentralized system:

- What is the difference between decentralized and distributed systems? (Industry Article)

- Difference Between Centralized, Decentralized & Distributed Systems Oversimplified (Industry Article)

(2) Advantages and disadvantages of a centralized system and a decentralized system:

Module 2 Technological and Cryptographic Elements in Blockchain

Welcome to Module 2

Dear Learners,

Welcome to Module 2 Technological and Cryptographic Elements in Blockchain.

In Module 1, learners had an overview of the advantages and disadvantages of a decentralised system and a centralised trusted party in processing, and storing transaction data and you also had a glimpse of some issues to be resolved in a decentralised system.

In Module 2, you will see how blockchain technology works. Blockchains are designed to be immutable. You will see how the cryptographic elements including public-private key pairs, digital signatures and hash values are at work to achieve the special properties of blockchain. In addition to hearing from chief instructor Dr Siu Ming Yiu, you will also meet our guest speaker Prasanna Mathiannal (Co-Founder of MaGEHold) later in the module.

Happy learning and have a great week.

HKU Blockchain and FinTech Course Team

Module 2 Learning Objectives

After completing Module 2, learners should be able to:

- understand the basic usages of three cryptographic elements, public-private key pair, digital signature, and hash value;

- understand how the three cryptographic elements are used in blockchain to guarantee the properties of blockchain, such as immutability and privacy;

- understand basically how blockchain works such as how a new transaction can be appended, how to achieve consensus of miners, and why a miner would like to help.

Video 2.1.1 Cryptographic Elements: Public Key & Private Key

- Welcome to Module 2 of our Blockchain course.

- In the last module,

- we have discussed two issues.

- The first one is why we need to have a blockchain.

- In particular, we do not want to have

- a centralised authority to handle our transactions.

- And then, the second issue is about the technical issues

- for having a blockchain, namely, the security,

- integrity, and the privacy issues.

- Now, so in this module, we start to look deeper

- into the technical elements of a blockchain

- and how these elements work

- together to form the blockchain.

- The first elements I want to talk about are the public key,

- private key, and digital signature.

- In fact, they are mainly used

- for encryption and decryptions.

- The public key and private key,

- they always go in pairs.

- So basically, each user will have a pair

- of public key and private key.

- The public key can be open to the public,

- so everybody can know your public key.

- But on the other hand,

- for the private key,

- we need to keep it secret.

- If you know one’s public key,

- you are not able to deduce his private key.

- So in other words,

- even if you can see people’s public key,

- it’s very, very difficult to deduce what his private key is.

- In encryption, how are we going to use this public key

- and private key pair?

- For example, if Alex wants to send

- an email or a document to Bob,

- so Bob is the receiver and Alex is the sender.

- Alex wants to keep the email confidential,

- so one way they can do it is:

- Alex tries to encrypt the document

- before it’s sent over through the internet.

- Now, then we try to use

- public key / private key encryption.

- Alex will use Bob’s public key to encrypt the document.

- So in other words, we are using the recipient

- or the receiver’s public key to encrypt the document.

- And once the document is encrypted,

- even if the hacker over the network can get a hold

- of your encrypted version of the document,

- he has no idea what will be the content.

- When the receiver, Bob, gets the

- encrypted message from Alex,

- he use his private key, then he’s able to decrypt

- the message to see the real content of the documents.

- So this is how the public key and private key

- can be used together in order

- to keep things confidential.

- So we try to use the receiver’s public key to encrypt

- the document and when the receiver receives

- that encrypted version of the document,

- he will use his own private key

- to decrypt the message

- inside the encrypted documents.

- And the important property is

- if you do not have the right private key,

- it’s very, very difficult to decrypt the message.

2.1.2 Cryptographic Elements: Digital Signature

- Now, the second concept, also very important

- in blockchain is called digital signature.

- Now, a digital signature basically is very similar

- to the physical signature we want to do on a document.

- But, right now, we just put it in the digital world.

- So if you’re given a digital document,

- what you can do is you can create a digital signature

- on that particular document, using your own private key.

- So when you sign a document,

- you used your own private key,

- because private keys and public keys,

- they go in pairs,

- so the corresponding public key can be used

- by others to verify your signature,

- see whether this signature is from the owner

- of the private key.

- Now, if you change even one character or just one bit

- in a document, the signature won’t match.

- So in other words, if the document has been changed,

- I can just verify the signature,

- and then the signature will tell you that

- this is not correct, it’s invalid.

- Then you know that the document has been modified

- and the signature is not correct anymore.

- So this is the second cryptographic element

- that is important for the construction of the blockchain.

- But then I want tell you an efficiency problem

- for digital signature.

- So, basically, for any document,

- you can also create a digital signature

- using your own private key.

- But, the problem is if the document is long,

- the signature that we created will be also long.

- So in other words, the longer the document is,

- the longer time to create the signature,

- and also the longer the signature will be.

- So this becomes an efficiency problem.

- If you want to send a document

- together with the signature,

- over from one side of the internet to the other side,

- then it wastes quite a lot of bandwidth

- if the document is large

- because the signature will

- become much larger in this case.

- How do people solve this problem?

- So we also have another technique,

- which is called the hash value.

- So given any digital document,

- no matter how long the document is,

- we can always generate a fingerprint of fixed length.

- For example, some of the

- common hash value generation

- will produce a 160-bit of a fingerprint for a document,

- no matter how long the document is.

- And this fingerprint, we give it a name

- called hash value, and this hash value

- has a very similar property as a digital signature.

- So if people try to change one bit, or one letter,

- in the document, the hash won’t match.

- So in other words, if I give you the document,

- together with the hash value and, actually,

- you can check whether the

- document has been changed or not.

- If the document has been

- changed the hash won’t match.

- Another key point is this hash function

- is not something secret.

- So, in other words,

- everybody knows how to calculate this hash.

- Or you can get a hold of a function

- to calculate this hash value,

- so if I give you the same document,

- everybody is going to create the same hash,

- using the same function.

- Now, so you can see that this hash value can serve

- as a fingerprint for the integrity of the document.

- So let me give you a quick example,

- so if I want to tell people that

- this is my document, D,

- and I want to tell people that

- this document, D,

- has not been changed by others.

- So what I can do is,

- I can send you the document, D,

- and then I create a hash value of D,

- and then send you the hash value as well.

- And after I send you the hash value,

- because I do not want other people

- to change the hash value,

- so I can tell people that this hash value

- is produced by me, so I can actually

- sign on the hash value.

- This gives us a very fast and safe way

- to send documents, over the internet,

- so that people cannot change it.

2.1.3 Cryptographic Elements: Real-life Scenario Challenges

- Let me give you a real example.

- If Alex is going to send a contract to a company X

- over the internet, if you just send a message,

- plain text over from Alex to the company X,

- basically the hacker has the capability

- to modify any content of the message.

- For example, they can pretend that the contract

- is not from Alex.

- They can change the name of Alex to Devil.

- And then try to send this message over to the company

- together with the contract.

- Then company X may think that

- the contract is from Devil,

- but not from Alex.

- To make sure that this won’t be able to happen,

- we can actually use the technique,

- what we have just talk about.

- Let me ask you a few questions,

- see whether you know how to answer these questions.

- If you know the answer to this question

- it means that you really understand this concept.

- So the first method is:

- So Alex tries to send over the contract C.

- And together with a hash value of the contract C.

- So do you think this is safe?

- Now if you think about it, this is not safe.

- The main reason is, if you still remember what I talked

- about, the hash value can be produced by everybody.

- So in other words, if the attacker gets a hold

- of your contract C, and the hash value of C,

- he is able to change the contract C into C-prime,

- and at the same time,

- re-compute another hash value

- for the C-prime and try to send the C-prime

- and the hash value of the C-prime

- over to the company X.

- When the company X gets a hold of

- the tampered contract C-prime

- and the hash value of C-prime,

- he has no way to discover that the

- contract has been changed.

- Because the hash of the C-prime

- will match with the tampered contact C-prime.

- So this won’t work.

- So you cannot just send the contract C

- plus the hash value over because the attacker

- is able to modify the contract and the hash

- at the same time, so that the receiver may not realise

- that the contract has been changed.

- So we need one more technique.

- Alex, should try to send three things over

- to the company X.

- First, he needs to send the contract C,

- and then the hash value of C,

- and also he has to sign on the hash value of C.

- So basically it’s the contract, the hash value,

- and the signature of the hash value.

- Now in this way, if you think about it carefully,

- even if the attacker gets a hold of these three content,

- he might be able to change the contract C to C-prime,

- and also he might be able to change the hash value of C

- into hash C-prime, but the problem is,

- he is not the owner of the private key, of the signature,

- so he is not able to sign on the hash value correctly.

- So in this case, then he is not able to change everything

- so that the receiver will not notice it.

- The receiver can verify the hash value

- and the signature to check whether the document

- has been tampered or not.

- So this is basically the way we need to make sure

- that the document has not been tampered.

- Now, let me ask you another question,

- see whether you really know how to answer it.

- Now, then how about another student may give me

- another answer saying, then how about Alex will try

- to just send a contract C

- and also sign on the contract C,

- and send the signature of the contract

- and the contract over to the company X.

- So do you think this is safe enough?

- From the security point of view, yes, it’s safe.

- Because even if the attacker

- get a hold of these two contents,

- he might be able to change the contract C to C-prime,

- but he cannot sign on it,

- because he is not the owner of the private key.

- And the receiver once can verify the signature,

- can know that the signature is not valid

- for the contract C-prime.

- So in other words, from the security point of view,

- this operation is okay, is safe.

- But I hope you still remember, if you make a signature

- directly on a document, then the size of the signature

- will be as big as the document.

- So in other words, you are wasting bandwidth

- in order to send a long contract together

- with a long signature.

REMARKS from Chief Instructor Dr SM Yiu

2.2.1 Cryptographic Technology: Key Questions for Blockchain

- Let’s focus back to blockchain.

- Now, for an easy understanding,

- let’s put blockchain in the context of bitcoins.

- Let’s talk about what is a transaction.

- As a simple example,

- a transaction is something like this.

- A person, A, tries to pass X bitcoins to B.

- For example, Alex may want to transfer 10 coins to Bob.

- Or Bob can transfer, six coins to David.

- All these – each one of them will be called a transaction.

- Now think, what’s a transaction chain?

- So it’s also very easy to understand.

- So a transaction chain is a sequence of transactions

- and they are ordered by the creation time

- of the transaction.

- Now, so at the beginning, you can assume that

- Alex has 20 coins and Bob only has one coin.

- And right now, Alex starts to transfer 10 coins to Bob,

- so this basically is one transaction.

- And after the transaction,

- then you can see that Alex will have 10 coins

- after transferring 10 coins to Bob

- then Bob will have 11 coins.

- And later on, Bob can also transfer

- six coins to David, but then for the transaction

- to be executed, usually, we need an authorization.

- For example, in a bank, we’re trying to ask Alex

- to sign on a transfer slip,

- so that the bank knows that it’s authorised by Alex

- to transfer 10 coins from Alex to Bob.

- And similarly, if Bob wants to transfer six coins to David,

- Bob also needs to sign on a transfer slip

- before the bank will try to make the transfer for Bob.

- And why do we trust the bank?

- The reason is very simple.

- Because the bank has a very comprehensive procedure

- and this procedure will be covered by the law,

- so that’s why we trust the bank to make sure that

- all the transactions are valid and correct.

- Now, but I want to remind you, in reality,

- even if the bank has a comprehensive procedure

- for every transaction, but then, some of its rules,

- basically, it still relies on the staff to follow them.

- So if the staff is cheating, in fact,

- there’s no 100% guarantee for the safety

- or the security of the transactions.